The recent bull market in gold left many analysts puzzled about the primary source driving the buying frenzy. However, it has become abundantly clear that the majority of the demand originates from China.

A recent report by The World Gold Council highlighted the following key points:

- The Shanghai Gold Benchmark PM (SHAUPM) in RMB jumped by 10% in March and the LBMA Gold Price AM in USD rose by 8%. The SHAUPM ended Q1 with a 10% gain, outperforming major local asset classes.

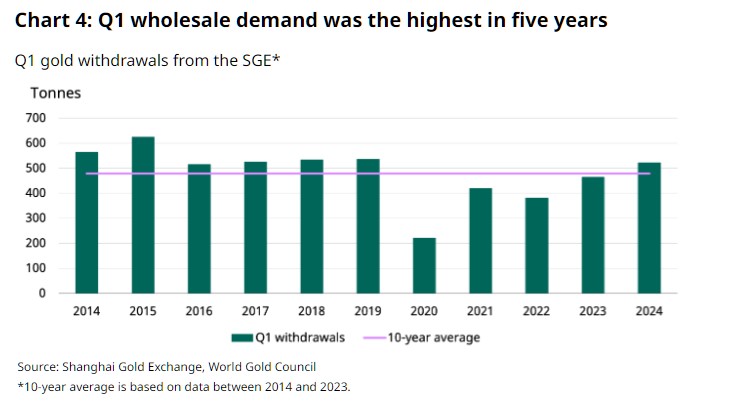

- 124t of gold left the Shanghai Gold Exchange (SGE) in March, a mild 3t fall from February as the surging gold price dented demand. But Q1 wholesale gold demand rose to its highest since 2019, totalling 522t.

- China’s gold price premium retreated in March, reflecting weakened local gold demand in the face of the soaring gold price. But the first quarter as a whole saw the highest Q1 premium ever (US$40/oz), driven by strong physical demand during the first two months.

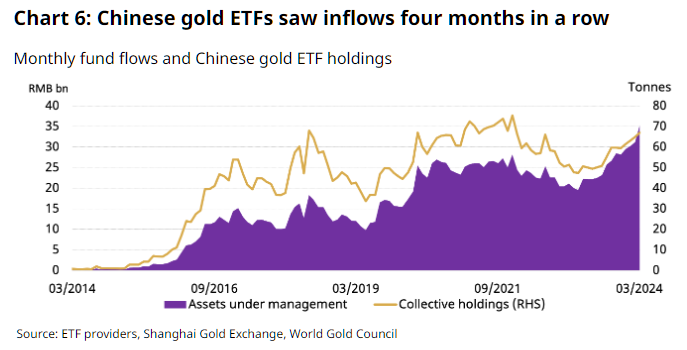

- Chinese gold ETFs continued to attract inflows, adding RMB1.2bn (+US$164mn) in the month and pushing total assets under management (AUM) to another record high of RMB35bn (US$5bn); March lifted Q1 inflows to RMB2.8bn (+US$386mn) and total AUM by 20%.

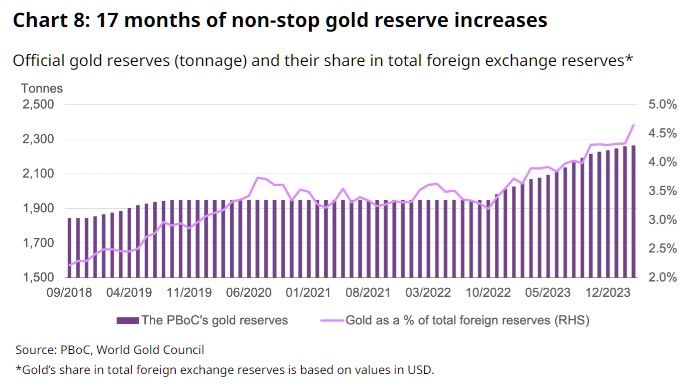

- The People’s Bank of China (PBoC) reported the 17th straight monthly purchase in March, adding 5t to its total gold holdings, which now stand at 2,262t or 4.6% of total reserves. China’s gold reserves increased by 27t in Q1.

China witnessed a surge in gold demand in the past quarter, reaching its highest level by weight in five years, as reported by data from the Shanghai Gold Exchange. Furthermore, as a proportion of China’s gross domestic product (GDP), gold demand hit a near-decade high, solidifying its position as the world’s leading gold-buying nation.

Despite reporting robust GDP growth last week, China’s economic landscape is facing challenges. The country’s property market is experiencing a downturn, the stock market has reached five-year lows, and cash interest rates remain historically low. In response, Chinese households and investors are turning to gold as a safe haven, contributing to the rapid rise in gold prices.

To meet this escalating demand, wholesale gold demand through the Shanghai Gold Exchange, the sole legal avenue for bullion to enter private circulation in China, surged by 12.3% in the first quarter compared to the same period in 2023. This marks the highest Q1 total since 2019 based on SGE withdrawals data.

The first quarter, encompassing the Lunar New Year and Spring Festival holiday, traditionally represents the peak gold-buying season globally, outpacing India’s autumn festival of Diwali. However, beyond seasonal gifting demand, the onset of 2024 witnessed a remarkable increase in private-sector investment in China, propelling the value of wholesale gold demand by 30.3% year-on-year. This surge surpassed Q1 2019 by 71.3% and accounted for 0.86% of the country’s GDP, marking the highest first-quarter proportion since 2015 according to analysis by BullionVault.

Amidst continued declines in China’s property sector, the first quarter of 2024 witnessed the CSI300 stock-market index plummeting to five-year lows, sinking to less than half its value compared to the peak of early 2021.

In stark contrast, Yuan gold prices soared by 10.1%, reaching new all-time record highs on 13 out of the first quarter’s 59 trading days at the Shanghai Gold Exchange (SGE). Furthermore, the quarter saw a record quarter-average premium of $40 per Troy ounce over London quotes, quintuple the typical incentive for new bullion imports.

The China Gold Association attributes this remarkable performance to the weakening of domestic assets such as equities and real estate. As a result, Chinese investors seeking safe-haven assets have continued to fuel demand for gold.

Retail-store demand for gold coins and small bars is experiencing a surge. Moreover, there is a growing enthusiasm among investors for gold investment through mobile and online banking platforms, including major platforms such as Ant Fortune, JD.com Finance, and Tencent Financial Management Connect. According to China’s Securities Times, “Gold prices are high, and trading is hot,” with speculative betting on gold prices through the Shanghai Futures Exchange also witnessing a significant increase in 2024. Chinese gold ETFs saw inflows for four months in a row.

But it’s not just Chinese investors increasing their gold positions. The Central Bank (PBOC) had 17 months of consecutive gold purchases.

In summary, the surge in gold demand witnessed in recent weeks has been primarily driven by factors such as economic uncertainties, weakening domestic assets like equities and real estate, and growing interest in safe-haven investments among Chinese investors. This surge in demand has led to record-high gold prices and increased trading activity in China’s gold market.

Furthermore, the strong retail-store demand for gold coins and bars, coupled with the growing trend of investing in gold through digital platforms, highlights the broad nature of the demand across multiple platforms in China. As China continues to play a significant role in the global gold market, its actions and investments will likely continue to influence gold prices and market dynamics worldwide, as the shift of gold from the west to the east is certainly playing out in recent months.

To follow our market commentary and more, create a free trading account online HERE.

Featured Product

Follow Us On Socials

![]()

![]()

Disclaimers: Guardian Gold, Registered Office, Scottish House, 100 William Street, Melbourne, Victoria, 3000. ACN 138618176 (“Guardian Vaults” & “Guardian Gold”) All rights reserved. Any reproduction, copying, or redistribution, in whole or in part, is prohibited without written permission from the publisher and/or the author. Information contained herein is believed to be reliable, but its accuracy cannot be guaranteed. It is not designed to meet your personal situation. Guardian Gold, its officers, agents, representatives and employees do not hold an Australian Financial Services License (AFSL), are not an authorised representative of an AFSL and otherwise are not qualified to provide you with advice of any kind in relation to financial products. If you require advice about a financial product, you should contact a properly licensed or authorised financial advisor. The information is indicative and general in nature only and is prepared for information purposes only and does not purport to contain all matters relevant to any particular investment. Subject to any terms implied by law and which cannot be excluded, Guardian Gold, shall not be liable for any errors, omissions, defects or misrepresentations (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (direct or indirect) suffered by persons who use or rely on such information. The opinions expressed herein are those of the publisher and/or the author and may not be representative of the opinions of Guardian Gold, its officers, agents, representatives and employees. Such information does not take into account the particular circumstances, investment objectives and needs for investment of any person, or purport to be comprehensive or constitute investment or financial product advice and should not be relied upon as such. Past performance is not indicative of future results. Due to various factors, including changing market conditions and/or laws the content may no longer be reflective of current opinions or positions. You should seek professional advice before you decide to invest or consider any action based on the information provided. If you do not agree with any of the above disclaimers, you should immediately cease viewing or making use of any of the information provided.