2022 Performance

Our gold and silver outlook 2023 report will take a look back at the year that was and look forward to some of the key fundamentals for next year’s precious metals market. When comparing financial market performance in 2022, gold and silver did relatively well, although many investors would have been hoping for better returns, given the level of uncertainty and geopolitical crisis during the year. At the time of writing (December 13th) gold in AUD terms is up 5.48% year to date, with silver the overachiever at +10.41% to date. In a nutshell the market benefitted from huge ETF inflows in the early part of the year on the back of the Russian invasion of Ukraine, only to give back all of those gains mid-year, to finish higher in AUD terms, and flat in USD terms.

The dust settled in the precious metals market in the middle of 2022, despite the war raging on without an end in sight. ETF inflows turned to net-outflow as many short-term traders exited the market in the first half. Metals ended up tracking sideways, helped along by an increase in physical investment demand, as well as strong central bank demand in regards to gold.

It is important to note that investors should be relatively happy with this performance, given the circumstances. The year saw interest rates rocketing higher at the fastest pace since the 1990’s, bond yields spiking and a flight to safety towards the US dollar. Crypto markets were absolutely obliterated, with market as a whole dropping 61% year-to-date, wiping out over $1.3 Trillion US dollars in market cap. US stocks dropped over 16% and the ASX is looking like finishing in the red for the year, currently down circa 5% YTD at time of writing.

It is important to note that investors should be relatively happy with this performance, given the circumstances. The year saw interest rates rocketing higher at the fastest pace since the 1990’s, bond yields spiking and a flight to safety towards the US dollar. Crypto markets were absolutely obliterated, with market as a whole dropping 61% year-to-date, wiping out over $1.3 Trillion US dollars in market cap. US stocks dropped over 16% and the ASX is looking like finishing in the red for the year, currently down circa 5% YTD at time of writing.

A turbulent year for financial markets and one in which there were far fewer asset classes in the green than in the red. The positive outtake for precious metals investors should be that despite all the chaos in markets in 2022, gold and silver have now formed a nice base to rally off as we move forward into next year. The market lows of July through September have been met with strong physical demand, and prices are already recovering despite central banks continuing their interest rate hiking cycle.

Our primary reason to be bullish in 2023 is based on the ‘unexpected’ pivot towards easier monetary policy by central banks, as their hand is forced by rapidly weakening economic conditions. Any excuse to put the brakes on the tightening cycle will likely be taken, and both gold and silver should benefit from the looser monetary policy to come. With the pace of interest rate hikes combining with high debt levels across governments, corporations and households, there is also a great potential for a major economic shock in 2023.

Secondly, physical investment demand continues to underpin the precious metals space and is growing rapidly. The Perth Mint broke their record monthly sales in October this year with their monthly gold sales being 206% higher than the same month last year.

With great uncertainty in 2023 to come, we think investors will continue to turn to the ultimate safe havens of gold and silver in an era riddled with economic challenges.

Geopolitical Uncertainty in 2023

Although geopolitical rallies in the gold price are often short-lived, there has to be an acknowledgment that geopolitical escalations and war can have long lasting economic consequences that influence both fiscal and monetary policy. We have seen the war in Ukraine leading to a spike in inflation across the globe, with central banks reacting quickly with tighter monetary policy. The two main concerns from a global geopolitical perspective in 2023 would be an escalation of Russian aggression and a potential conflict in Taiwan, involving the US, NATO and China.

Ukraine

The war in Ukraine is entering somewhat of a stalemate with Russia losing ground whilst targeting civilian infrastructure and Ukraine gaining the upper hand on the ground. There is still some risk of escalation and the main concern would be a potential nuclear situation, especially if Ukraine begin to target Russian positions inside Russian territory in the future. In general, when it comes to financial markets, we think the risks are being underappreciated by investors and we are basically in a position where markets are pricing in a slow grinding end to the war. Anything that goes against this assumption will likely see some large moves in markets in 2023. The “Ukraine premium” in the gold price has been taken our entirely, as the market traded back below levels seen before the invasion. This tells us that gold will unlikely react negatively to an end to the war, and likely very positively to any escalation.

Taiwan

The US has warned recently that a conflict over Taiwan would trigger a huge global economic shock. The state department shared research that a Chinese blockade of Taiwan would spark around $2.5 Trillion in annual economic losses. Taiwan is a major manufacturing hub for silicon computer chips with the largest chip maker in the world being TSMC. TSMC recently announced that they’ll be moving their most advanced manufacturing to Arizona, USA. The pressure put on Taiwan by China makes a lot more sense when you understand the importance of the computer chip superiority race between the US and China in years to come.

There will be a strategic battle underway for chip supremacy in future years, from both an economic and defense perspective, and TSMC is the world’s leading manufacturer. The importance of TSMC is also potentially a major reason why the US said it would intervene if China attempted to take Taiwan back by force.

With chip technology improving on an exponential scale, there will be a major importance on semiconductor chip technology and manufacturing in 2023 and beyond. Should China make moves in 2023 to claim Taiwan back by force, we would see a significant impact on the global economy which will be felt all over the developed world.

Central Bank Gold Demand Reaching Record Highs

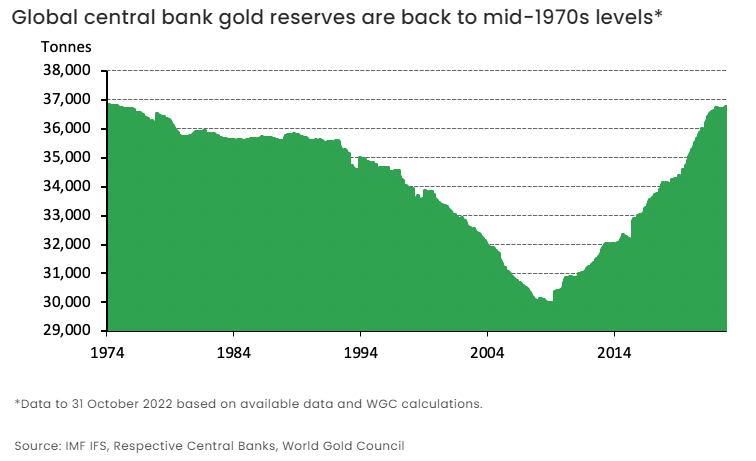

The World Gold Council reports that Central Banks continued to accumulate gold at a fast pace in 2022. The latest data from October saw central banks adding a further net 31 tonnes of gold to their international reserves, bringing total global gold reserves to its highest level since 1974. The central bank of UAE was the largest purchaser in October, adding 9 tonnes to its gold reserves.

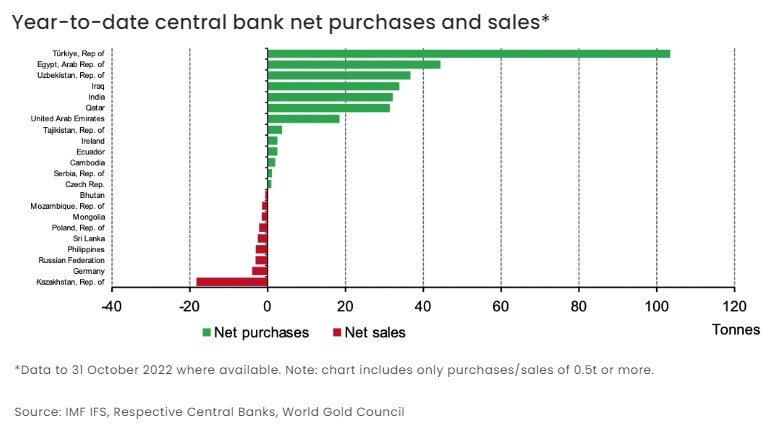

The Central Bank of Turkey was the largest purchaser of the yellow metal this year, adding 103 tonnes of gold to their balance sheet. Overall, central bank demand in the third quarter of 2022 far exceeded the previous quarterly record stretching back since data began in 2000. The trend of strong net-purchases of gold by central banks is expected to continue in 2023, which should help gold price fundamentals. Improving central bank demand is a strong indicator of long-lasting support for gold, as ETF speculators can flip from one asset class to another, whereas central banks are much more long-term focused and unlikely sell their positions in a short time frame.

Electric vehicle demand to help silver fundamentals

Although silver doesn’t receive the same benefit from central bank demand as gold does, there is one important growing market for industrial demand that is unique to silver and not gold. That is the electric vehicle (EV) market and the trend moving forward towards 2030.

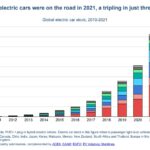

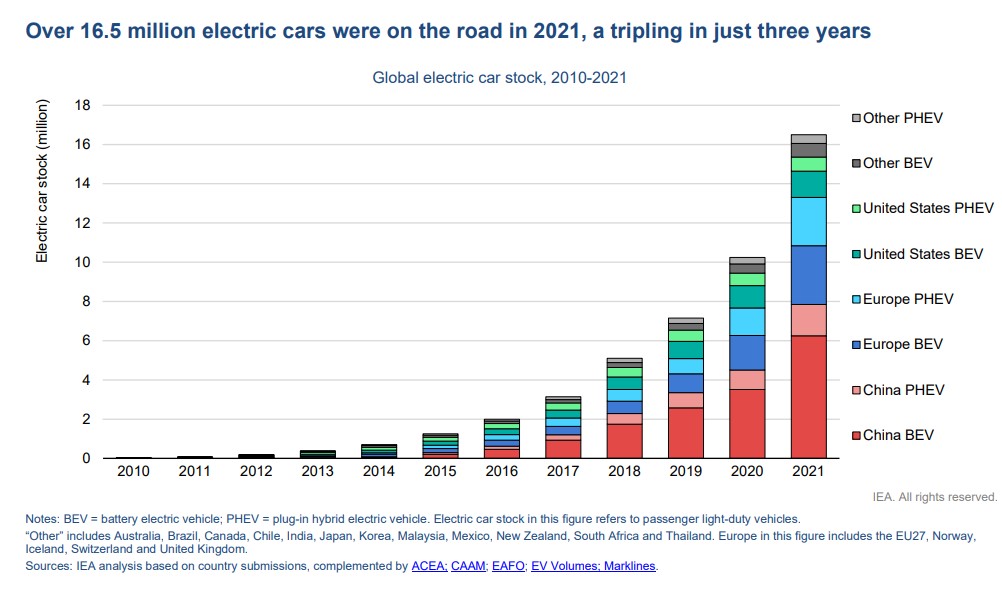

EV sales are on track to hit an all-time high this year and the strong trend of manufacturers switching their models from internal combustion engines (ICE) to electric motors in undeniable. Over 16.5 million EVs were on the road in 2021, which is a tripling in just three years.

The amount of silver in each electric vehicle is said to be around one ounce, or between 25-50 grams per vehicle. Now this doesn’t sound like a lot at first, but when you consider the major trend here and compare with annual global silver demand and supply as a whole, it is actually quite a significant amount and large enough to see supply deficits.

Annual sales of EV’s is estimated to grow to around 26 million cars per year in 2030. This would equate to circa 26 million ounces (over 808 metric tonnes) of additional silver demand per year just from new car sales. Not to mention demand from additional components or replacement of parts as almost every electrical connection in an EV uses silver. The Silver Institute project total silver consumption by the automotive market to increase to over 90million ounces by 2025, and growing beyond this in 2030.

If other demand factors such as renewable energy industrial demand and investment demand continue to gain traction as we move towards 2030, we could see a big enough supply deficit in the silver market to start seeing a positive and lasting impact on the price. Industrial demand factors for silver in the years to come seems to be on positive footing with solar PV investment and initiatives also boosting demand for the physical metal.

Watch Out for the Central Bank Pivot in 2023!

The all-important tightening cycle for central banks could well end in 2023, despite many forecasters suggesting otherwise. The general consensus today is that inflation will persist into 2023 and that central banks will continue to hike rates to combat it. The problem is; central banks will soon be faced with a dilemma of dealing with a severe economic slowdown and global recession due to the strain of higher debt servicing costs impacting economic activity.

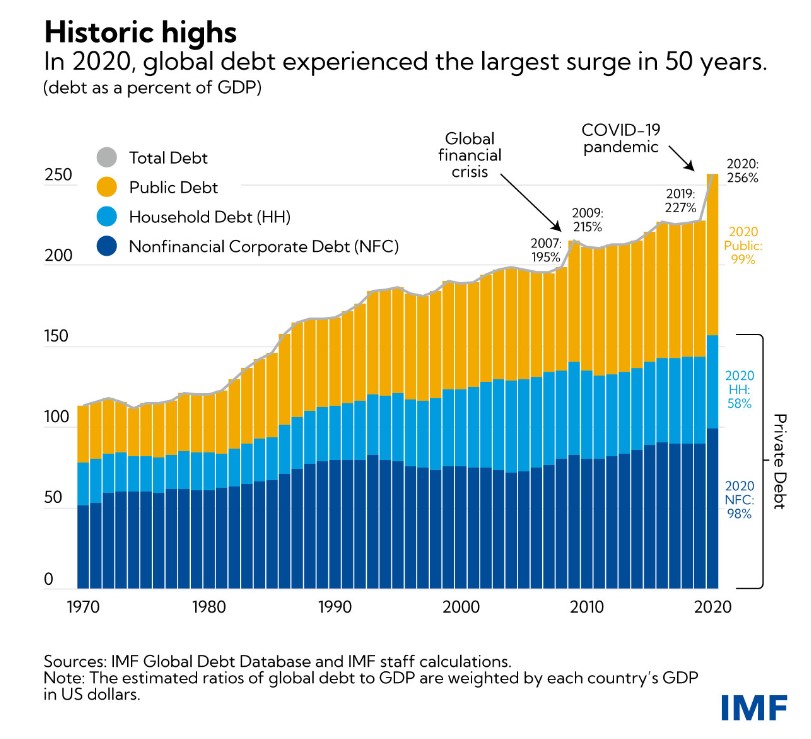

Credit rating agency S&P Global recently warned that world debt is more highly leveraged than before the 2008 financial crisis. Corporations, individuals and governments have loaded up on record debt during the zero-interest rate policy (ZIRP) years up until 2020. The rating agency also highlighted the massive debt carried by China’s corporate sector, estimated at US$27 Trillion and growing.

A lot of this debt is soon to reset to much higher interest rates, with Australia’s household debt a perfect example. A total of $99 billion worth of Aussie mortgages are coming off fixed rate positions in the second half of 2023. Many of these borrowers will be looking at significant jumps in their mortgage repayments which will put negative pressure on consumer spending, economic growth and likely property prices. Forced selling of some properties may add to supply as those mortgage holders without a savings buffer might not afford the higher rates.

A lot of this debt is soon to reset to much higher interest rates, with Australia’s household debt a perfect example. A total of $99 billion worth of Aussie mortgages are coming off fixed rate positions in the second half of 2023. Many of these borrowers will be looking at significant jumps in their mortgage repayments which will put negative pressure on consumer spending, economic growth and likely property prices. Forced selling of some properties may add to supply as those mortgage holders without a savings buffer might not afford the higher rates.

The dilemma of tackling inflation VS preventing an economic crisis will be a major challenge for central banks in 2023. We think there is a good chance that central banks will pivot back to easier monetary policy should economies start spiraling into crisis under the heavy burden of higher interest rates. We’d also expect gold and silver to catch a decent bid in this scenario if we see signs of central bank easing becoming a theme much sooner than most expect. Watch out for signs early on in 2023 of central banks putting the breaks on rate hikes and starting with dovish commentary.

Summary and forecasts

In summary, we see some very positive fundamentals underpinning both gold and silver in 2023. Property markets appear to be at risk of further falls. Equities are a mixed bag with selection of sectors being very important, and the government bond market could benefit with gold in 2023 if central banks start to pivot earlier than expected.

In regards to forecasts, we won’t throw darts at the price and try to guess a year-end outcome for 2023, but we can cover a few notable predictions from other analysts, including one prediction which should put a smile on the face of our fellow gold bulls.

Let’s start (of course) with the most bullish of forecasts. Ole Hansen, Head of Commodity Strategy at SAXO bank sees gold rocketing to $3,000 USD in 2023 as central banks fail on their inflation mandate. Hansen notes “2023 is the year that the market finally discovers that inflation is set to remain ablaze for the foreseeable future. Gold slices through the double top near USD 2,075 as if it wasn’t there and hurtles to at least USD 3,000 next year. ”

Bank of America expect gold to head past $2,000 in the later half of 2023 on the back of the Federal Reserve slowing interest rate hikes. CBA analyst Vivek Dhar see gold reaching $1750 – $1900 USD next year on the assumption the US dollar has now topped. ING’s commodity strategist also sees gold higher next year, trading up through $1,850 USD. Most analysts seeing more reasons for higher prices than lower ones, even with Natixis Investment bank economist quoting ‘I am hard pressed to see what could really drive gold prices lower next year’ despite having a neutral /bearish outlook of $1,600 USD lows.

2023 Gold Price Forecasts

- SAXO – $3,000+ USD

- Bank of America – $2,000 USD

- CBA – tops of $1,900 USD

- ING – $1,850 USD

Despite seeing robust growth in physical bullion demand in 2022, we still see gold and silver as under-owned asset classes. The trend of gold and silver investment is definitely a positive one, and we see a great opportunity for the market to grow further from here, given how few investors actually have gold or silver exposure in their portfolios. With the world more leveraged with debt than before the 2008 global financial crisis, we can’t see a scenario where central banks continue to raise interest rates without drastic consequences. 2023 could well be the year where markets rush towards the safety and security of precious metals, amid yet another crisis brought about by too much debt facing a major rate hike cycle.

Disclaimers: Guardian Gold, Registered Office, Scottish House, 100 William Street, Melbourne, Victoria, 3000. ACN 138618176 (“Guardian Vaults” & “Guardian Gold”) All rights reserved. Any reproduction, copying, or redistribution, in whole or in part, is prohibited without written permission from the publisher and/or the author. Information contained herein is believed to be reliable, but its accuracy cannot be guaranteed. It is not designed to meet your personal situation. Guardian Gold, its officers, agents, representatives and employees do not hold an Australian Financial Services License (AFSL), are not an authorised representative of an AFSL and otherwise are not qualified to provide you with advice of any kind in relation to financial products. If you require advice about a financial product, you should contact a properly licensed or authorised financial advisor. The information is indicative and general in nature only and is prepared for information purposes only and does not purport to contain all matters relevant to any particular investment. Subject to any terms implied by law and which cannot be excluded, Guardian Gold, shall not be liable for any errors, omissions, defects or misrepresentations (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (direct or indirect) suffered by persons who use or rely on such information. The opinions expressed herein are those of the publisher and/or the author and may not be representative of the opinions of Guardian Gold, its officers, agents, representatives and employees. Such information does not take into account the particular circumstances, investment objectives and needs for investment of any person, or purport to be comprehensive or constitute investment or financial product advice and should not be relied upon as such. Past performance is not indicative of future results. Due to various factors, including changing market conditions and/or laws the content may no longer be reflective of current opinions or positions. You should seek professional advice before you decide to invest or consider any action based on the information provided. If you do not agree with any of the above disclaimers, you should immediately cease viewing or making use of any of the information provided.